I’ve been asked to speak to the All Party Parliamentary Group on Forestry and Tree Planting today. This is what I’m planning to say:

Last time I presented to you I talked about the benefits of using home-grown timber and why tree planting alone will not provide the benefits we desire. This time I am going to talk about the hardwood and specialty softwood market. The extent of it, the part home grown plays and what the future holds. I will also urge you to ensure that we plant trees with purpose and set out a National Timber strategy to provide the raw material we will need in future.

Imports and ambitions

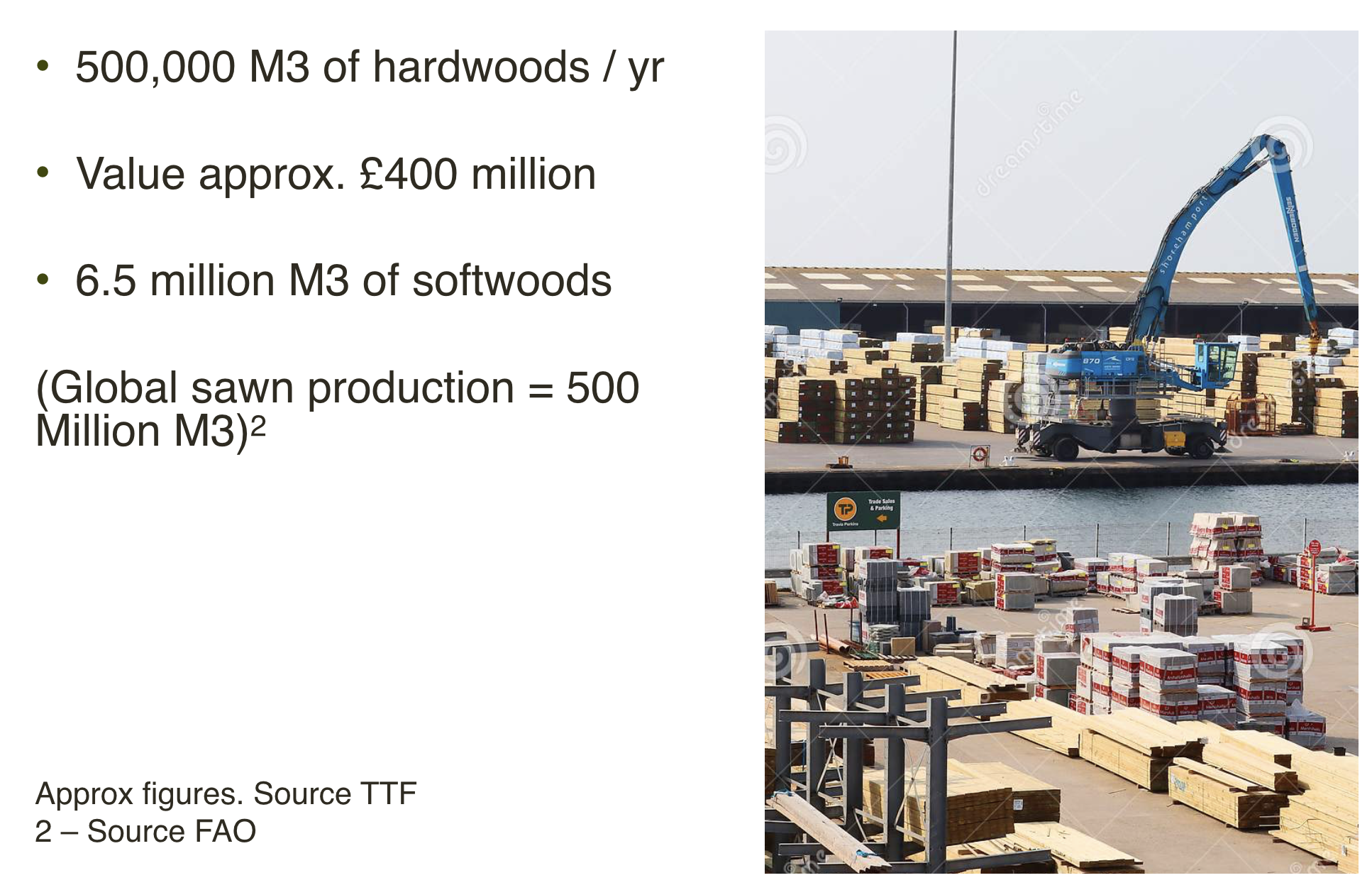

We import approximately half a million M3 of hardwoods each year, and our biggest supplier is the US. The purchase value is around £400 million. To put that in context we import approx. 6.5 million M3 of softwoods and total global sawn timber production is 500 Million M3.

In the UK we produce approximately 25,000 – 35,000 M3 of hardwood timber from 76,000 green tonnes of hardwood logs. About 7% of the total used. To put that into context, about ten times this amount ends up as woodfuel.

I was asked to talk about my ambition. In truth there isn’t much room for ambition. We simply don’t have the quantity or the quality of standing timber for too much ambition. We have relatively little broadleaf and mixed woodland and only a small proportion of that is commercially viable. We can do a bit better with what we have but believe me, there is no big untapped resource out there.

I do have a lot of frustration because we are embarking on an exciting bio based revolution with wood due to play a starring role. As a country we are making bold pledges to cut emissions, 11% of which come from the production and installation of building materials.

Wood is an obvious replacement for carbon intensive and non-renewable building materials. But we simply don’t have much of it. We haven’t taken forestry seriously in England for forty years at least.

Now you have listened to enough of these presentations to know most of what I have told you, but you won’t know the next bit. What I am going to tell you now is not based on future predictions of hope or gloom it is reality and it’s happening now.

Up until now we have been able to import 70% of our timber needs in the UK and over 90% of the hardwoods we use without too much trouble. Remember that we are the second biggest timber importer behind China.

That’s changed. There’s a United States building boom, and the US is our largest hardwood supplier. The US Lumber futures market recently rose from $300 to $1300 (/1000 bdft). There’s also an Australian building boom, a Chinese building boom, and on top of that, reduced cutting due to pest damage and historic over-cutting. Meanwhile freight rates from Asia up by a factor of four in just 6 months.

The timber ‘taps’ have turned off!

A few real examples of the effects include Danzer, which normally imports 800m3 Sapele per month, is down to 400m3. Timber Connections, which normally stocks 400M3 of 27mm AM White oak is down to 60M3. There is almost no Canadian cedar available to buy, and prices are rising dramatically across the board.

Some of these specific drivers I mentioned will ease but the macro trends will make things tougher for the UK, a country that relies on importing 70% of its timber.

Let’s think more generally about timber. Because in reality it is a false dichotomy to talk about hardwoods and softwoods as separate choices.

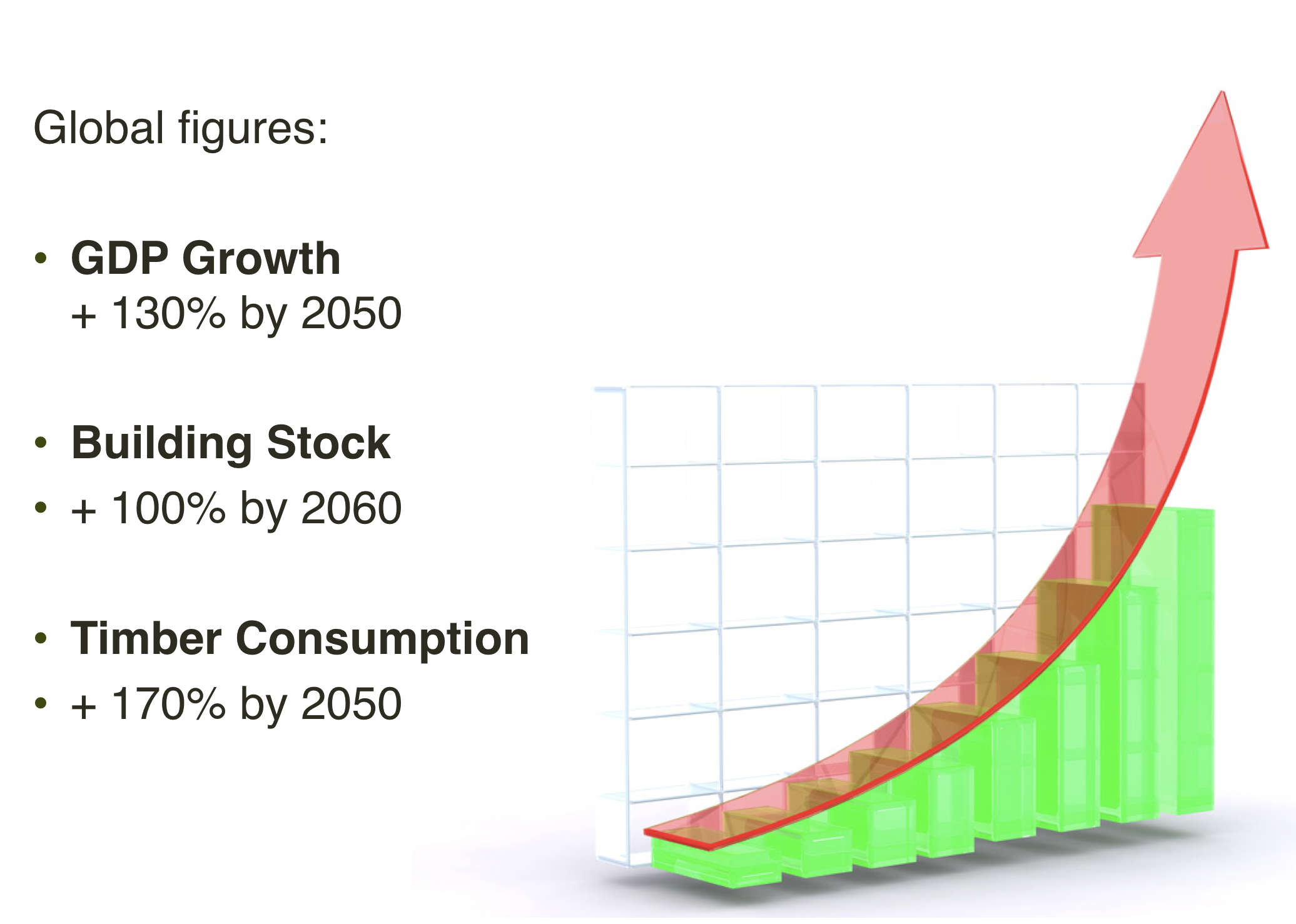

Global predictions put GDP growth at 130% by 2050, building stock up 100% by 2060, and timber consumption up 170% by 2050 (2.2 Billion M3 to 5.8 Billion M3 round wood consumption)

(Sources – 2.2 Billion figure Food and agriculture Organisation & Gresham House, 5.8 Billion figure – Gresham House)

(Sources – 2.2 Billion figure Food and agriculture Organisation & Gresham House, 5.8 Billion figure – Gresham House)

The increased demand for timber is driven by urbanisation, housing demand and decarbonization. However by 2050 available volumes of round wood will be in the region of 3.7 to 4.7 billion M3. Which means that between now and then demand and supply will part company. Timber will become ever scarcer. Countries that have it will undoubtedly want to hold on to it.

We need a national timber strategy

We have a problem and I am afraid that failure is baked in for the next forty years. The severity of this situation is equivalent to that which the country faced after the great war. Timber is an essential commodity and it is in very short supply.

What we need is a National Timber Strategy, similar to that of 1919 when the Forestry Commission was created.

“In September 1919, the Forestry Commission was established by the Forestry Act to undertake a tree planting mission of truly epic scale, replanting our woodlands, creating a future supply of home-grown timber and providing thousands of jobs for demobilised servicemen.”

Now, over 100 years after that strategy launched, The Climate Change Committee’s 6th carbon budget calls for a scaling up of afforestation rates to 30,000 hectares a year by 2025. This is in line with the UK Government’s commitment, rising to 50,000 hectares annually by 2035. This would increase woodland cover from 13% of UK land area to around 18% by 2050.

This ambition gives us a scale, but it says nothing about quality of planting, ongoing management or the usefulness of the woodlands, forests and the timber resource in the future.

This epic challenge calls for the next National Timber Strategy

A Strategy that :-

• Replaces the current paralysis

• Acknowledges the scale of the challenge

• Takes responsibility for producing renewable and clean building products and plastic replacements of the future

• Lays down a timber crop for 2060 onwards

• Includes native hardwoods, naturalised hardwoods, valuable conifers such as cedar and Douglas fir, productive areas of spruce and pine as well as experimental species.

• Insists on selected seed and ongoing management

If we are going to plant all of these trees, let us not waste the opportunity. I urge you to ensure that we plant with purpose and set out with a strategy. And provide the raw material for ambition in the future.

Thank you for listening.